The AASB S2 Climate-related Disclosures.

5 April 2025

Sustainability reporting in Australia

Up until 2025, sustainability reporting in Australia comprised of voluntary reporting by larger organisations and mandatory reporting under the National Greenhouse and Energy Reporting (NGER) Scheme for high emitters.

With the introduction of the ASRS, we now have an expanded and significantly more structured reporting regime.

The Australian Sustainability Reporting Standard (ASRS) was finalized and published in September 2024.

It can be downloaded at:

https://standards.aasb.gov.au/sites/default/files/2024-10/AASBS2_09-24.pdf

The ASRS has been developed by the Australian Accounting Standards Board (AASB) and are also referred to as the AASB S2 Climate-related Disclosures.

The ASRS is the practical detail behind the broader Climate-related Financial Disclosure legislation which was passed into law on 9 September 2024.

In summary, the above legislation introduces the requirement for certain organisations to include climate-related disclosures in their general purpose financial reports.

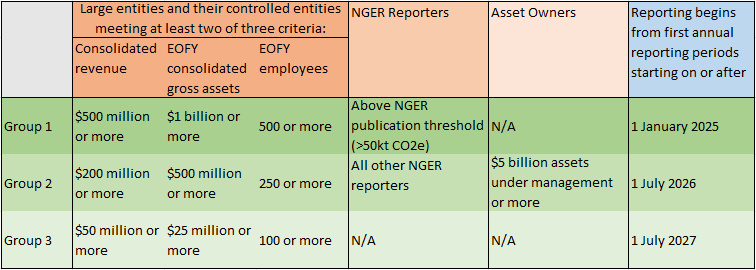

The requirements will be phased into effect as per below table:

The requirements fall into two broad categories:

1. Big-picture type reviews and statements around climate-related risks and strategy as identified by each reporting organisation.

2. Detailed annual report outlining measured or estimated greenhouse gas emissions as per GHG Protocol.

The big-picture items will make use of the data collected and calculated in the detailed reports, and will require some environmental science input, but for the purpose of the ASRS report, these items are primarily a finance and general management activity and responsibility.

The detailed reports will include all Scope 1,2 & 3 emissions related to the operation of the organisation, including the entire value chain. This means that organisations will need to consider emissions caused by their suppliers, distributors and clients.

The concept of measuring or estimating emissions from 3rd parties will be a new and complex challenge for most organisations. In some cases, there may be a need to ask suppliers for emissions-related data in order to meet this reporting requirement.

The difference between NGER and ASRS

The simple answer is that ASRS includes the NGER emissions and adds material Scope 3 emissions plus a whole bunch mandatory commentary. For existing NGER reporters, they will continue to submit NGER reports, there is no change to that regime, but they will now need to add Scope 3 emissions to their ASRS emissions report.

Entities who are required to prepare ASRS reports but have not and do not need to prepare NGER reports, will now have to calculate their Scope 1, 2 & 3 emissions for ASRS.

Another important difference is that NGER reports are “environmental” reports and must be prepared according to the very detailed and technical NGER legislation, the ASRS reports are “financial reports” and need to speak to general stakeholders in the entity, primarily existing and potential shareholders.

The practical reality of the ASRS reporting requirements

As covered above, the core of the ASRS is the emissions inventory and estimated emissions for the reporting entity. However, it is worth emphasising that the ASRS is primarily a communications activity.

The intent and purpose of and ASRS is to provide clear and comparable information about the existing state of emissions, planned emission reduction actions and climate-related risks to the operations of the entity, and most importantly, how these are likely to financially impact the entity.

The preparation of an ASRS report will need to be a collaborative exercise, it will require input and decision-making from the board of directors, the executive team, the finance team and either an internal or external environmental team. For a lot of entities, there will also be a significant input and interest from the marketing/communications teams.

Critically, it will also need to have an increasing level of assurance (audit).